Rule of 78 |

|

|

|

|

||

|

Rule of 78 |

|

|

|

|

|

Rule of 78

|

Rule of 78 |

|

|

|

|

||

|

Rule of 78 |

|

|

|

|

|

|

|

||

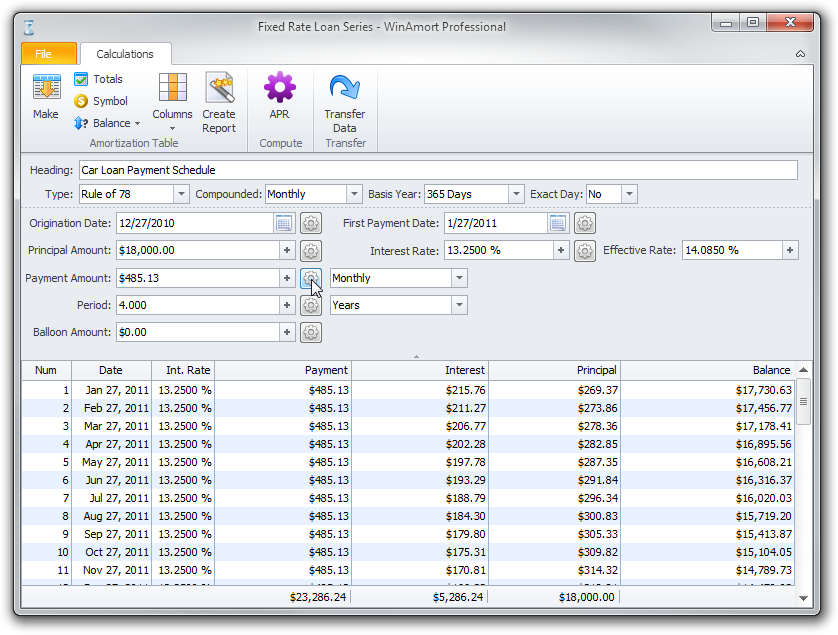

The set-up of the Rule of 78 screen is identical to that of the Normal loan type. Even the calculations on the form will be the same. The difference arises when an amortization table is created. In a Rule of 78 loan, a larger amount of interest is charged at the beginning of the loan and this amount decreases as the loan progresses. The total interest charge is the same as that for a Normal loan. In cases where a loan is paid off early, the lender benefits because of the higher interest charges at the beginning.

Your form should look like this.

The table is automatically generated when you click the Payment Amount Compute button.

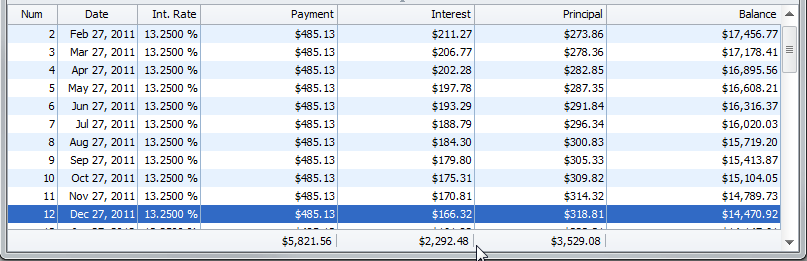

Scroll down the table using the side bar or the wheel on your mouse and click on Dec. 27, 2012 (this is line number 12) and notice, that the total interest for the first year is $2,292.48 and principal balance is $14,470.92.

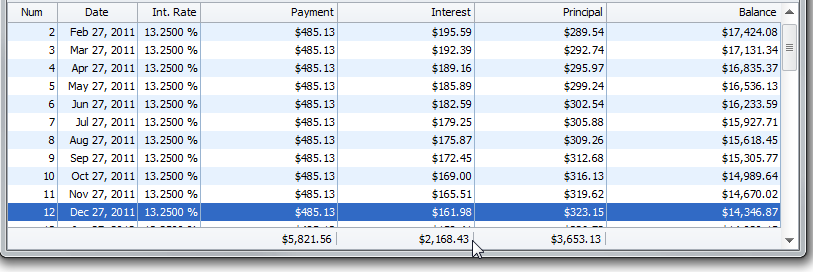

Now let's compare these values with a REGULAR LOAN type, by generating another table.

Change the Option for loan type from RULE OF 78 to

Once the NEW table is generated again, scroll down to line 12 again and click on it.

This time, the first year’s interest for this table is $2,168.43 and the principal balance is $14,346.87.

When you compare these values to the Rule of 78 values, we had first year interest of $2,292.48 and a principal balance of $14,470.92 .

The difference between the Normal loan type and the Rule of 78 loan type is that $124.05 more interest is paid in the Rule of 78 loan. Although, if you compare the total interest cost at the end of the loan for both loan types, it will be equal.

What this shows is that the Rule of 78 Loan type has been designed to collect more interest earlier or up front and less interest towards the end of the amortization period. There is no difference to the borrower or the lender if the loan is paid regularly up to the end of the amortization period. However, if the borrower decides to pay off the loan earlier, the Rule of 78 loan benefits the lender because more interest has been collected early.

Goto: Fixed Principal

|